Article

Decoding Market Moves for C-Suite Leaders Amidst the Microchips War

As the world’s two largest economies face off over the microchips war, every move—whether a government-imposed ban or a strategic investment—sends ripples through the industry. The recent ban on Micron Technology by China, following a series of US sanctions, marks a significant escalation in this tech war, one that is set to redefine market dynamics and supply chain strategies globally. In this critical juncture, where geopolitical tensions and technological advancements collide, CTOs must decode these market shifts with precision.

This article will delve into the roots of the chip conflict, explore its ramifications on the semiconductor industry, and offer strategic insights for navigating this tumultuous landscape.

The genesis of Sino-American microchips conflict

The US-China semiconductor clash has its roots in the broader technological rivalry between the two nations. The US’s technological offensive began with a series of export control bans implemented in October 2022. These restrictions targeted Chinese semiconductor firms, notably Yangtze Memory Technologies Corp., Semiconductor Manufacturing International Corporation (SMIC), and HiSilicon. The goal was to limit China’s access to advanced semiconductor technologies and halt its progress in key areas like artificial intelligence (AI) and high-performance computing.

The US strategy was supported by allies, including Japan, Taiwan, and the Netherlands, who imposed informal bans on technology exports to Chinese firms. This collective action significantly disrupted China’s semiconductor supply chain, creating a substantial gap in its ability to procure and produce advanced chips.

In response, China has taken a definitive retaliatory step by banning Micron Technology, the largest US memory chipmaker, from supplying products to critical national infrastructure operators in China.

This decision followed a seven-week investigation by the Cyberspace Administration of China (CAC), which concluded that Micron’s products posed “significant security risks” to China’s critical information infrastructure.

The ban, which came against the backdrop of the G-7 summit’s call to de-risk technology supply chains and Micron’s $3.6 billion investment in Japan, is China’s first major retaliatory move. This action marks China’s significant retaliatory measure in the chip war, highlighting the strategic importance of its domestic market.

[Image Source: Citi Group]

Implications of Sino-us chip war for the semiconductor industry

China’s semiconductor industry, though currently accounting for only 16 percentage of global production, is rapidly evolving. In memory chips, China’s share is notable, with 21 percent in dynamic random-access memory (DRAM) and 15 percent in NAND. Despite these figures, China remains heavily reliant on foreign technology for high-end chips, especially those requiring advanced lithography tools from ASML, a Dutch company.

In response to the US sanctions, China has intensified its efforts to bolster domestic capabilities. For instance, the Chinese government has injected $1.9 billion into Yangtze Memory Technologies Corp. (YMTC), aiming to enhance its competitive edge against global giants like Samsung and SK Hynix. Additionally, firms like Powev Electronic Technology Co. are scaling up production, indicating a strategic push towards self-reliance.

The immediate beneficiaries of Micron’s ban are Chinese memory chip manufacturers, including Ingenic, CXMT, YMTC, and GigaDevice. These companies are positioned to capitalize on the reduced competition in the domestic market. Conversely, Micron faces potential revenue losses and a decline in market share. The company’s withdrawal from critical infrastructure segments could lead to a broader erosion of its market presence in China.

Market data snapshot:

- Micron’s market presence: China is Micron’s third-largest market. The company’s revenue from China was approximately $3.7 billion in 2022, making this market critical for its global operations.

- Competitors’ position: South Korean firms Samsung and SK Hynix, which together hold a significant share of the global memory chip market, are poised to benefit from Micron’s exclusion. Samsung holds a 43 percent market share in DRAM and a 21-percent share in NAND as of 2023, while SK Hynix controls about 29 percent of the DRAM market and 18 percent of NAND.

Considerations for CTOs to sail through the supply chain disruption

The semiconductor supply chain is increasingly fraught with geopolitical risks. The global supply chain of semiconductors is estimated to involve over $500 billion annually. A disruption in this chain can have cascading effects across multiple industries, emphasizing the need for resilient supply chain strategies.

CTOs need to reassess their supply chain strategies to mitigate potential disruptions. Key strategies include developing a diverse supplier base to reduce dependency on any single region or provider, implementing robust risk management frameworks to anticipate and address potential supply chain disruptions.

Leveraging domestic investments

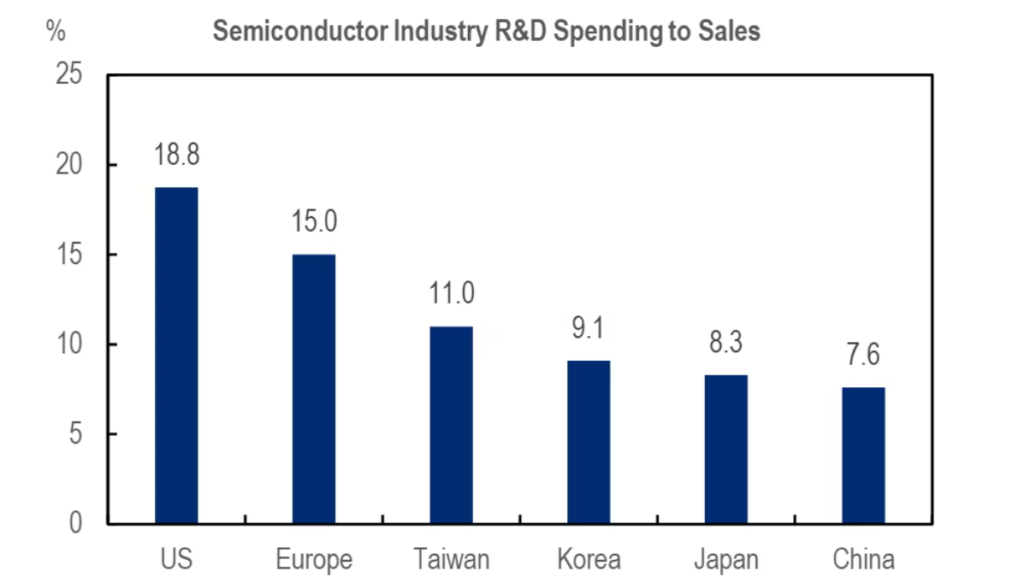

The US CHIPS and Science Act, aimed at bolstering domestic semiconductor production, presents both opportunities and challenges. The CHIPS Act allocates $52.7 billion over five years for domestic semiconductor manufacturing and R&D.

However, the cost of establishing a state-of-the-art fab is estimated between $10 billion and $40 billion, highlighting the significant investment required. However, these programs face significant challenges, including higher costs and regulatory hurdles. CTOs should evaluate the potential benefits and risks associated with domestic investments in semiconductor manufacturing, considering both financial and operational implications.

Adapting to market shifts

TSMC dominates the global foundry market with a 58 percent share. Its expansion efforts, including new fabs in the US, will significantly impact global chip supply dynamics. Samsung’s established foundry business and its 27 years of experience in the US position it to benefit from new domestic manufacturing incentives.

The rapid changes in the semiconductor landscape necessitate agile strategies for technology leaders. Keeping abreast of developments in domestic chip manufacturing capabilities, understanding shifts in global supply chains, and leveraging new investment opportunities will be key to maintaining a competitive edge.

In brief

The Sino-US chip war is a complex and evolving saga with far-reaching implications for the global technology sector. For C-suite leaders, particularly CTOs, navigating this landscape requires a nuanced understanding of geopolitical dynamics, strategic investment opportunities, and supply chain risks. As the chip conflict unfolds, staying informed and adaptable will be crucial in steering through the uncertainties and capitalizing on emerging opportunities in this high-stakes arena.