{kind=link}

Neobank 3.0: How AI-Driven Challenger Banks Are Building Smarter, Leaner Financial Platforms

In the quiet but fast-accelerating revolution of financial services, a new wave of banks is reshaping everything we thought we knew about consumer finance. These are not just banks without branches; they are agile, AI-native platforms engineered for scale, speed, and deep personalization. Welcome to Neobank 3.0.

Over the past decade, nearly 400 licensed neobanks, digital-only, cloud-native challengers to traditional banks, have launched globally. These startups, often born out of fintech innovation, have targeted the inefficiencies of legacy banking with precision.

Their premise is simple: deliver better, cheaper, more personalized financial services. But as macroeconomic pressures intensify, and investor expectations shift from growth to profitability, only a select few have found the formula to scale sustainably.

What sets these winners apart? Increasingly, it’s not just technology. It’s how they are using artificial intelligence to redesign the banking model from the ground up.

Neo Bank and the shift to AI-powered financial intelligence

Licensed neobanks like Revolut, Chime, and KakaoBank have demonstrated that rapid growth is possible. But growth without sustainable profit is no longer sufficient in today’s environment of rising interest rates, tighter regulatory scrutiny, and cautious capital. The future belongs to AI-first banks, those that deeply embed machine learning into everything from product development to risk management.

These banks are not merely digitizing legacy processes. They are rebuilding the financial stack to enable faster decisions, personalized services, and automated operations. The goal? Customer-centricity at scale—and at a fraction of the cost of traditional institutions.

Hyper-personalization in finance: a new paradigm for customer engagement

AI-driven personalization is now fundamental to consumer trust and retention in digital finance. Leading neobanks are abandoning the one-size-fits-all product model in favor of n = 1 hyper-personalization in finance, the idea that every user should receive a unique financial journey based on their individual behavior, context, and needs.

Instead of just recommending new credit products, these banks predict life moments—job changes, travel, or budgeting stress—and surface contextual offerings. Klarna, for example, uses machine learning to tailor shopping and financing offers based on user preferences, integrating seamlessly into consumers’ digital habits.

For CTOs building or overseeing platform architecture, the challenge is twofold:

- Building the data infrastructure to unify behavioral, transactional, and contextual data

- Deploying scalable AI models that serve unique outputs at the customer level in real time

This type of micro-targeted delivery is redefining loyalty. It’s no longer about brand affinity; it’s about behavioral relevance.

AI-powered compliance tools are quietly transforming risk and regulation

Compliance has long been a bottleneck for financial innovation. But now, AI in banking is disrupting its most rigid domain: regulation. Emerging AI-powered compliance tools are changing how digital banks monitor fraud, assess risk, and meet regulatory obligations at scale.

WeBank in China uses AI to resolve 98 percent of customer queries without human intervention, demonstrating not just cost efficiency but compliance through automation. In the U.S., Chime leverages open banking protocols to provide real-time account aggregation, making transparency both a feature and a safeguard.

Modern compliance is no longer retrospective. With AI tools, it’s predictive.

This shift has critical implications for CTOs. AI now governs transaction scrutiny, monitors for AML flags, and generates audit trails, essentially building “compliance by design” into the core product. This doesn’t just mitigate risk; it accelerates product deployment cycles once mired by regulatory review.

The invisible force: decision-making engines beneath the UX

Behind every tap on a mobile banking app lies a growing network of decision-making models, algorithms predicting creditworthiness, optimizing offers, and even flagging fatigue in user engagement.

This AI-and-analytics-led decisioning layer sits between the user interface and the core banking system. Its purpose? To orchestrate a real-time response to every user input and behavioral signal. Models are tuned not just for performance but for ethics and explainability, a necessity in a post-GDPR, AI-skeptical world.

Leading neobanks treat this layer not as a back-office function but as a strategic advantage. It drives the what, when, and how of all product delivery.

For technical leaders, this calls for deeper integration across data science, engineering, and product teams, dissolving traditional silos and enabling a culture of continuous learning and rapid iteration.

Architecting for scale: the role of modular tech and open APIs

Scalability in Neobank 3.0 is not about bigger infrastructure. It’s about modular, microservices-driven architecture that can pivot, adapt, and scale horizontally. That means decoupled services, API-first development, and elastic cloud infrastructure built for rapid product experimentation.

Chime, for example, uses API integrations (via Plaid and others) to connect external accounts within its own app, a seamless user experience that boosts engagement and transactional volume. Notably, customers who link external accounts spend 5x more through Chime’s debit cards, according to the company.

These modular systems also allow for AI experimentation at the edge, meaning banks can A/B test models in live environments without destabilizing the core stack. For CTOs, this design principle is fast becoming a blueprint for agile financial infrastructure.

Six defining traits of successful AI-first neobanks

1. Product innovation at breakneck speed

Neobanks are setting a new standard for how quickly financial products can go from idea to market. Unlike legacy banks, which often require years to launch a new service, firms like Revolut have engineered their tech stacks to enable continuous, agile product development.

Revolut, which launched in 2015 with a single travel card, now offers more than 20 distinct financial products, from cryptocurrency trading to business banking. This relentless pace is powered by full-stack teams—designers, data scientists, and legal and risk professionals- working in tandem and supported by modular technology that accelerates testing and deployment.

2. Customer engagement as core currency

The best neobanks treat engagement like equity. Beyond offering competitive pricing, they design experiences to keep users interacting with their platforms, often daily. Think of gamified budgeting tools, dynamic shopping rewards, and interactive financial content.

Klarna, the Swedish payments platform, exemplifies this with AI-driven product recommendations and personalized shopping insights embedded directly into its app.

By cultivating digital intimacy, these platforms move closer to the holy grail of banking: becoming the daily financial operating system for customers.

3. Conversational interfaces replacing bureaucracy

Traditional banking portals are being replaced with intelligent, chat-based interfaces. Whether via chatbots, voice assistants, or video consultations, leading neobanks are moving toward natural language as the primary mode of interaction.

WeBank in China, a pioneer in this space, reports that nearly 98% of its customer service requests are now resolved by AI. It is enabling it to serve millions without dramatically expanding its workforce.

4. Open banking, built in from day one

Rather than treat open banking as a compliance obligation, the most forward-looking neobanks see it as a design principle. Built with API-first architectures, they allow users to connect accounts across institutions, creating a unified financial view that fosters loyalty and engagement.

Chime, through its partnership with Plaid, enables users to aggregate external accounts into its app. According to internal data, customers who link an external bank account spend up to five times more through their Chime debit cards.

5. Embedded ecosystems through strategic partnerships

AI-powered neobanks are not just building standalone apps—they are embedding banking functionality into the broader digital ecosystem. Whether through social media, e-commerce, or mobility platforms, the idea is simple: meet users where they already are.

KakaoBank, formed by South Korea’s dominant messaging platform KakaoTalk, has integrated banking into a vast digital suite—from rideshare to gaming. As of late 2021, the bank had over 18 million customers, demonstrating the power of distribution through digital partnerships.

6. Customer lifetime value as the new North Star

Successful neobanks are rethinking performance metrics. Instead of focusing solely on interest margins or cost-to-income ratios, they emphasize customer lifetime value (LTV), acquisition costs (CAC), and return on investment per user.

Cash App, owned by Block Inc., reportedly breaks even on new users within six months and earns six times its CAC by month 18. This granular, cohort-based analysis helps the company tune everything from marketing to product development with surgical precision.

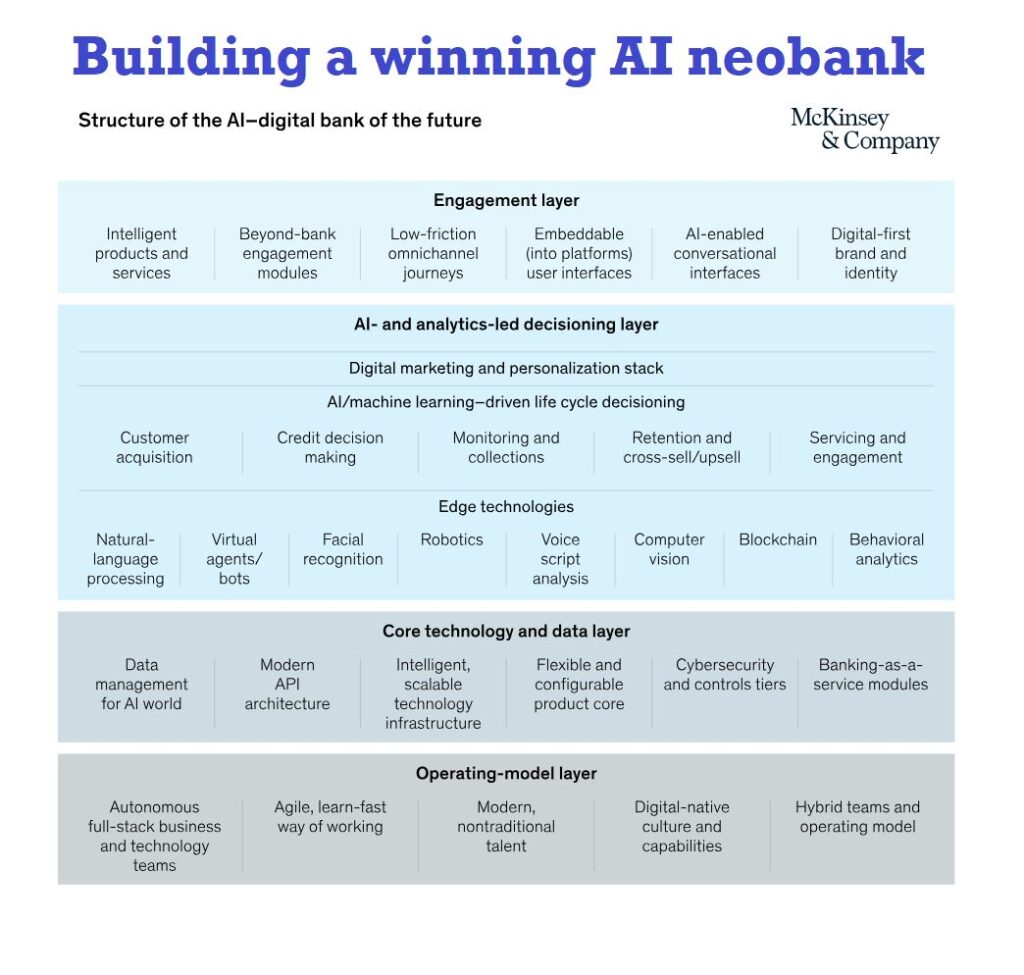

The four-layer framework for the AI-driven neobank

To build a next-generation digital bank, firms must align strategy and execution across four interdependent layers:

- Engagement layer

Where user experience lives, this includes seamless mobile journeys, hyper-personalized nudges, and context-aware integrations with third-party ecosystems.

- AI-led Decision-making layer

The brain of the bank. It powers everything from credit risk to customer retention through dozens of machine learning models fed by real-time data streams.

- Cloud-native tech and data layer

The infrastructure. Cloud-first, microservices-led platforms allow rapid scalability, while unified data lakes support real-time analytics and AI deployment.

- Operating model layer

The organization itself. Full-stack teams, agile governance, and a culture of experimentation empower neobanks to move faster than incumbents, while still adhering to regulatory rigor.

Banking’s future is modular, behavioral, and intelligent

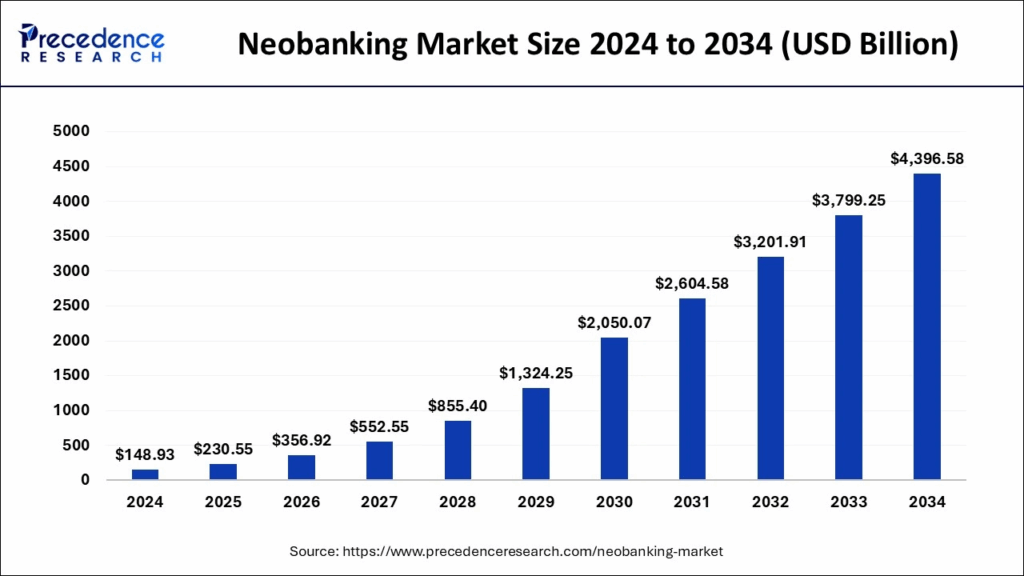

The appeal of neobanks remains strong. By 2032, Neo Bank is predicted to grow to an to an estimated value of USD 3,02,025.3 million. Global venture funding continues to flow, though more selectively than in past years.

But the market is maturing. The era of easy growth is giving way to one that rewards strategic clarity, disciplined execution, and above all, intelligent systems.

The winners of this new phase—Neobank 3.0, will not be the flashiest or the most aggressive. They will be the most adaptable, the most data-native, and the most relentlessly focused on building AI-powered banking models that are lean, trusted, and ultimately profitable.

In the end, the digital banking revolution is not about replacing tellers with touch screens. It’s about building institutions that learn, evolve, and serve with precision, at internet speed.

Neobank 3.0 is not a passing trend. It’s the blueprint for the next decade of financial services.

For CTOs and technology leaders, the takeaways are strategic and immediate:

- Build for modularity.

- Architect for learning.

- Invest in AI as both infrastructure and intelligence.

- Treat personalization as a product, not a feature.

And most of all—view compliance, engagement, and risk not as constraints, but as levers in the evolving operating model of intelligent, leaner banks.

Because the future of finance isn’t just digital, it’s decisively AI-native.

In brief

Neobank 3.0 is redefining digital banking—leaner, faster, and built on AI. Today’s top challenger banks are using AI-powered compliance tools, hyper-personalization in finance, and modular mobile banking apps to scale smarter and serve users more intuitively. For CTOs, this marks a shift from building tech to architecting intelligence across every banking layer.