{kind=link}

How AI Fraud Detection Became Banking’s Invisible Firewall

AI fraud detection is rapidly becoming the most critical layer of protection in modern financial systems. As digital transactions scale and threats become more complex, traditional fraud controls are insufficient.

Behind the scenes of this ongoing battle, artificial intelligence quietly acts as a watchful guardian.

Today, financial institutions face highly coordinated, fast-moving attacks that can slip past static rules and manual reviews. Consumer trust is on the line, and so is institutional credibility. Artificial intelligence is stepping in as the silent watchdog: scanning billions of data points, detecting subtle anomalies, and stopping fraud before it starts.

In this article, we’ll explore how AI-powered fraud detection is outpacing traditional methods by offering flexible, scalable protection.

How AI is transforming fraud detection in banking and commerce

Legacy fraud detection relied on fixed thresholds and manual checks—effective in a simpler era, but easily outpaced by today’s adaptive fraud techniques.

Modern fraud is dynamic: synthetic identities, account takeovers, and cross-border scams all operate at scale. Traditional tools miss these evolving patterns.

AI fraud detection addresses this gap with real-time analysis, behavioral modeling, and self-learning algorithms. It doesn’t just detect known threats, it anticipates unknown ones by constantly refining its understanding of user behavior and transactional context.

This proactive approach allows financial systems to respond within milliseconds, reducing false positives and preventing losses before they occur.

Common financial fraud: A closer look

In a landscape where fraudsters innovate daily, AI isn’t just helpful, it’s essential. And the institutions investing in advanced AI capabilities today are building a more resilient, trusted digital financial future. Financial fraud takes many shapes and forms, each with unique tricks and consequences. In our digital world, knowing how these scams work is more important than ever.

Identity theft

This happens when criminals steal personal info—things like Social Security numbers or credit card details—to pretend to be someone else and commit fraud. Usually, identity theft starts with data breaches, phishing scams, or stealing physical documents. The damage can be serious, from unauthorized charges to long-term harm to your credit score.

Subscribe to our bi-weekly newsletter

Get the latest trends, insights, and strategies delivered straight to your inbox.

Phishing and social engineering

Phishing scams rely on fooling people. Fraudsters pretend to be trusted entities—banks, government offices, or popular companies, to coax victims into handing over sensitive data. These scams can result in hacked accounts and unauthorized spending. The “Nigerian Prince” scam, or “419 scam,” is a classic example, where scammers pose as foreign royalty needing financial help. Though old, it’s adapted to new technologies and remains effective.

Payment fraud

Payment fraud involves stealing money through credit cards, digital wallets, or bank accounts without permission. This covers credit card fraud, wire fraud, and account takeovers, where someone gains control of your account to make fake transactions. In 2023, check fraud made a comeback, with thieves stealing and altering checks—showing that even old methods aren’t safe.

Investment scams

These scams promise big returns but deliver nothing. Pyramid schemes, fake crypto platforms, and “get-rich-quick” offers fall into this category. A rising threat is the “Pig Butchering” scam, where scammers build fake relationships online to persuade victims to pour money into bogus crypto investments, costing billions globally.

Insurance and loan fraud

Here, fraudsters file false insurance claims or fake loan applications to make money. They might exaggerate damages or submit forged papers to secure loans, raising costs for honest people and complicating lending. Sometimes, fake job ads gather personal data used to open fake bank accounts and get loans.

Money laundering

Money laundering disguises illegal funds by moving them through multiple accounts or shell companies to make the money look legit. This helps organized crime flourish and harms the economy. The “Black Axe” group, for example, uses complex laundering schemes involving unsuspecting people as drug mules.

Cyber fraud

Cyber fraud covers digital crimes like hacking, ransomware, and malware targeting financial systems and personal data. These attacks can shut down businesses and cause huge losses. The 2017 Equifax breach exposed data for over 147 million people, sparking many fraud attempts afterward.

The Bernard Madoff case that shook Wall Street

Few fraud cases have left a mark as deep as Bernard Madoff’s Ponzi scheme. Once a respected financier and NASDAQ chairman, Madoff orchestrated the largest fraud in history, defrauding investors of an estimated $65 billion.

Madoff promised steady, high returns through his investment firm. But instead of legitimate profits, he used money from new investors to pay returns to earlier clients. This illusion of success attracted more investments and sustained the scheme for years.

The house of cards began to fall in 2008 during the global financial crisis, when a surge in withdrawal requests revealed that funds were insufficient. Madoff was arrested in December that year.

Thousands of individuals, charities, and institutions lost significant sums. Charities and retirement funds were wiped out, highlighting the widespread damage caused by one man’s deception.

In 2009, Madoff was sentenced to 150 years in prison. Trustees continue working to recover lost funds, clawing back billions from those who unknowingly profited.

The Madoff scandal underscores the critical importance of due diligence, transparency, and oversight. It remains a stark reminder of how trust can be exploited—and why modern tools like AI-driven fraud detection are essential to safeguard the financial system.

How AI is fighting fraud: Success stories from banks worldwide

All over the world, banks and financial firms are putting AI fraud detection systems to work—and the results are impressive. What used to be a promising idea has become a practical, powerful tool protecting both institutions and their customers from increasingly clever fraud schemes.

Global bank implementations

Take JPMorgan Chase, for example. Their AI platform, called COiN (Contract Intelligence), was initially built to speed up the review of commercial loan documents. However, it also doubles as a fraud detector, spotting suspicious irregularities in contracts that could indicate fraud. This system can analyze thousands of documents in seconds, a job that used to take humans hundreds of thousands of hours every year.

Bank of America has “Erica,” an AI assistant that blends customer service with real-time fraud monitoring. By constantly tracking transaction patterns and alerting users to unusual activity instantly, Erica has helped prevent millions in potential fraud losses—all while boosting customer trust.

HSBC teamed up with AI company Quantexa to develop a fraud detection tool that looks beyond individual transactions.

Regional banking successes

AI benefits aren’t limited to big banks. Eastern Bank, America’s oldest as well as largest mutual bank, reported a drop in fraud losses and a 67% decrease in false positives within the first year of adopting AI. This proves you can strengthen security without disrupting the customer experience.

In the Netherlands, Rabobank has tackled authorized push payment (APP) fraud using AI to detect suspicious transaction patterns, account behavior, and timing. Since implementing AI, Rabobank has prevented about €80 million in potential fraud each year.

Credit card fraud prevention

Credit card fraud detection is one of AI’s most mature uses in banking. Mastercard’s Decision Intelligence platform processes over 1.3 billion transactions daily, analyzing more than 200 variables per authorization request. This system has cut false declines in half while improving fraud detection, a rare and valuable balance between security and convenience.

American Express uses AI to rapidly evaluate transactions, approving or declining purchases within milliseconds. The organizations AI-driven system reportedly saves the company $2 billion annually in fraud losses, while keeping the buying process smooth for genuine customers. These examples highlight how AI boosts both efficiency and customer satisfaction.

Mobile banking security

As mobile banking grows, AI tools tailored to this channel have become essential. UK-based Monzo Bank uses AI to watch in-app behaviors like typing rhythm and navigation, helping catch early signs of account takeovers.

In Spain, BBVA applies AI to analyze device data, user behavior, and location information to stop mobile banking fraud. These efforts have significantly cut fraud attempts, helping keep customer accounts safer.

Together, these real-world examples show how AI is reshaping banking security. From the largest institutions to regional banks, AI is helping protect assets and provide seamless, trustworthy experiences—an encouraging trend likely to grow in the years ahead.

Peering ahead: The next wave of AI fraud detection innovations in fintech

As fraudsters become increasingly sophisticated, the landscape of fraud detection is evolving at a rapid pace. Cutting-edge technologies and new strategies are emerging to help banks stay one step ahead of criminals.

Quantum computing

With its immense processing power, quantum technology could analyze vast and complex transaction datasets almost instantly. It is spotting hidden patterns that classical computers might miss.

While widespread quantum computing is still on the horizon, banks are already preparing by developing algorithms that will be ready to harness this technology once it matures. When fully realized, quantum-powered AI could detect coordinated fraud schemes operating across global networks at unprecedented speeds.

Federated learning

Strict privacy regulations, data-sharing restrictions have long posed challenges for banks aiming to collaborate on fraud detection. Federated learning offers a clever workaround. They have enabled multiple institutions to train a shared AI model without exposing any raw customer data.

This approach usually boosts fraud detection across the industry while respecting privacy laws such as GDPR and CCPA. Several banking consortia are already piloting federated learning projects with promising results, proving that collective intelligence can outperform isolated efforts.

Explainable AI (XAI)

As AI models become more complex. Their decision-making can seem like a “black box,” making it tough for regulators, also for customers to understand why certain transactions get flagged.

Explainable AI seeks to change that by making AI’s reasoning clear and transparent.

By offering detailed justifications for flagged activities, XAI helps investigators validate alerts faster and supports compliance with regulatory requirements.

Multimodal fraud detection

Traditional fraud systems tend to rely on one type of data—usually transaction records. The future lies in combining multiple data sources at once: transaction details, voice signals during calls, typing patterns, geolocation, even document images.

By integrating these diverse data streams, multimodal AI creates a fuller picture of suspicious behavior. It is improving accuracy and reducing false alarms.

Continuous authentication

Rather than relying on a single login check, continuous authentication uses AI to monitor user behavior throughout an entire session—tracking mouse movements, typing cadence, navigation paths, transaction timing, and more.

If the system detects unusual activity, it can prompt for additional verification or block risky actions. This persistent vigilance helps stop fraud attempts even after the initial login.

Synthetic identity detection

Synthetic identity fraud, where criminals create fake identities by blending real and fabricated data. It is a growing challenge and notoriously hard to catch.

Advanced AI models tackle this by cross-referencing fragmented information across databases to spot inconsistencies and patterns.

From vision to victory: CTO’s Roadmap for AI-driven fraud prevention

1: Assessment & foundation

- Objectives: Map fraud landscape and pain points; evaluate data readiness; build a cross-functional team.

- Actions: Conduct fraud risk audits; inventory and cleanse data; define KPIs such as detection rate and false positives.

- Success Metrics: Completed risk assessment, data readiness report, team charter, and defined KPIs.

2: Pilot & proof of concept

- Objectives: Choose AI tools aligned to scale; test models on historical and live data; validate accuracy and transparency.

- Actions: Pilot tools like Feedzai, Featurespace ARIC, or DataVisor; integrate behavioral biometrics if applicable; run parallel legacy system tests; involve legal early for compliance checks.

- Success Metrics: Improved detection accuracy (20%+ reduction in false positives), compliance alignment, pilot completion.

3: Integration and scaling

- Objectives: Fully integrate AI with existing security; automate workflows; embed Explainable AI.

- Actions: Implement multi-factor authentication; create real-time dashboards; schedule regular retraining; launch training programs to foster security culture.

- Success Metrics: Seamless AI adoption, reduced manual reviews, higher fraud mitigation, and positive user feedback on usability.

4: Continuous optimization

- Objectives: Track evolving fraud tactics as well as explore new technologies and strengthen ethical governance.

- Actions: Conduct fraud simulations, adapt to regulatory shifts. Pilot continuous authentication and multimodal data fusion; report progress to leadership.

- Success Metrics: Sustained fraud loss reduction, maintained compliance, demonstrable ethical AI practices, executive engagement.

Strategic Recommendations for CTOs

- Champion cross-team collaboration, bridging IT, legal, compliance, and customer experience.

- Prioritize transparency by adopting Explainable AI to foster trust inside and outside the organization.

- Invest in talent skilled in AI ethics, fraud patterns, and security.

- Balance aggressive innovation with privacy-by-design and compliance from day one.

- Treat AI models as living systems requiring constant adaptation to outpace fraudsters.

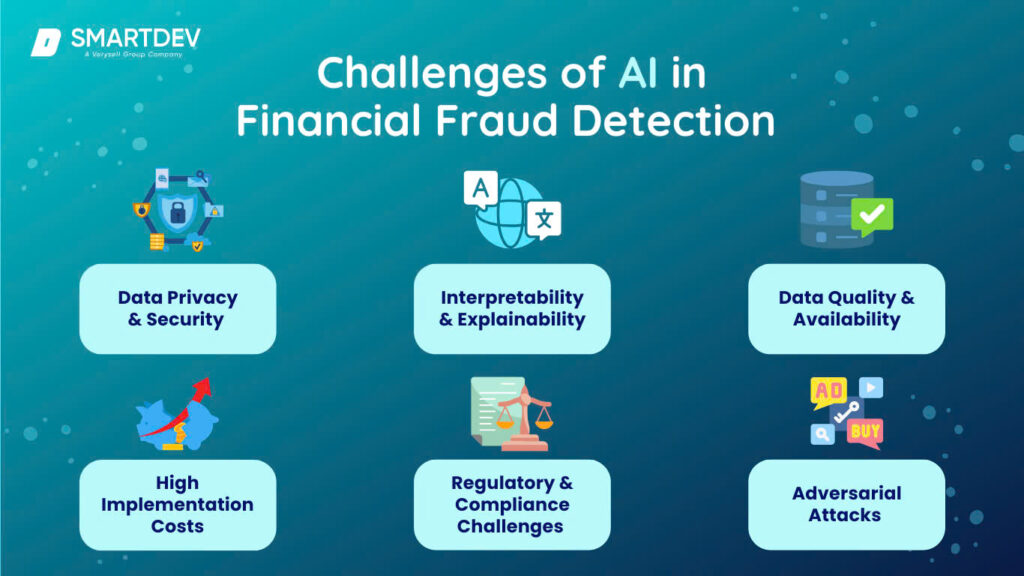

The complex realities of AI fraud detection

AI fraud detection wields enormous power but carries inherent challenges. Its success hinges on data quality, yet biases risk reinforcing unfair outcomes. CTOs must ask how to prevent models from perpetuating systemic inequities and what controls exist to audit these risks.

The “black box” nature of AI clashes with the need for transparency in fraud decisions. Striking a balance between model sophistication and explainability remains a pressing hurdle. Are current Explainable AI tools enough to meet regulatory demands without sacrificing performance?

Technology alone cannot solve fraud. Effective defenses rely on a security-conscious culture and collaboration across functions. CTOs should consider how to align security, compliance, and user experience, and empower teams to complement AI with human insight.

Moreover, ethical use and privacy add further layers of complexity amid shifting regulations. Building AI that respects privacy while also fostering trust—and anticipating future legal requirements—is absolutely paramount.

Questions every CTO should ask

- Can AI really do its job well if it’s not supported by multiple layers of security?

- How confident are we that our AI systems are fair and comply with all regulations?

- How do we keep up with rapid AI advances while making sure we’re acting ethically?

- Are our AI models tough enough to handle deliberate attempts to fool or hack them?

- What are we doing now to prepare for the fraud threats we haven’t even seen yet?

In brief

AI’s role in fraud detection is only set to grow. Acting like an invisible guardian, AI helps protect the integrity of modern finance by analyzing data in real time, spotting unusual behavior, and uncovering hidden patterns. But it’s not a magic fix, success requires careful oversight, strong ethical guidance, and constant fine-tuning to stay ahead of evolving threats.