{kind=link}

The Fintech Big Tech Convergence: How Google, Apple, and Amazon Are Quietly Becoming Banks

For decades, banking meant vaults, credit officers, and marble columns. But today, finance lives in your pocket, embedded in apps you use every day. Also, in an era of mobile devices, algorithmic decision-making, and digital ecosystems, we’re witnessing a seismic shift in the financial world. The lines between finance and technology are dissolving—what industry insiders now call the fintech big tech convergence.

This convergence isn’t about tech companies becoming banks in the legal sense. Rather, it’s about transforming how financial services are delivered, accessed, and understood. At the heart of this shift are the usual suspects in Silicon Valley: Apple, Google, and Amazon.

Fintech big tech convergence: A quiet revolution in plain sight

The fintech big tech convergence isn’t heralded with splashy announcements. It’s happening subtly, step-by-step, buried inside software updates and partnership press releases. Yet the implications are far-reaching: new forms of credit, seamless mobile payments, reimagined lending models, and user-first savings tools, all powered by platforms that already dominate our digital lives.

This convergence is redefining the future of financial services, and CTOs across the fintech and banking landscape are watching closely. Why? Because the game has changed. The competition isn’t just banks versus fintech anymore. It’s the platform economy versus everyone else.

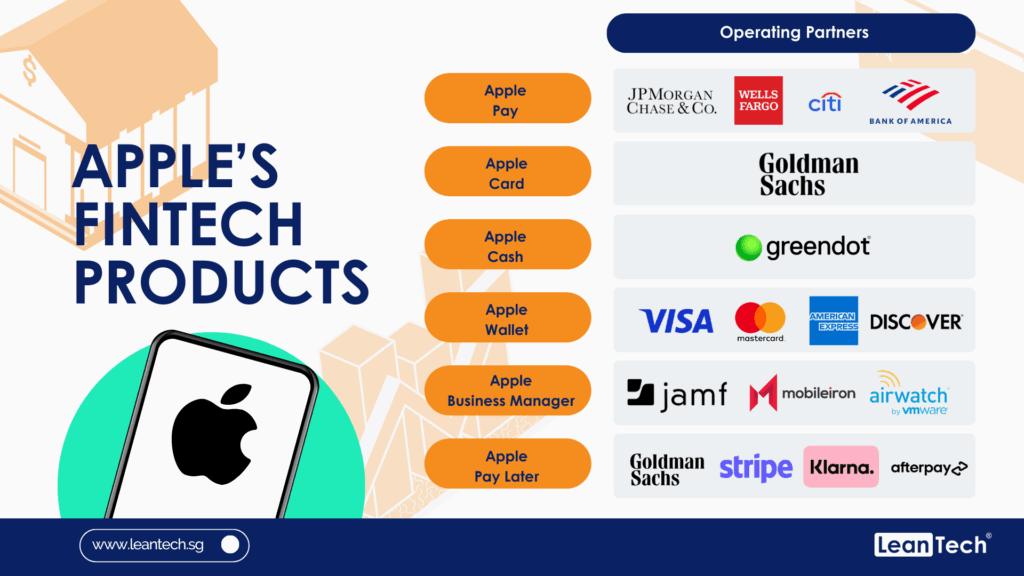

Apple: The core of the fintech big tech convergence

When Apple introduced the Apple Card in 2019, many saw it as a sleek new credit product. Few recognized it as the opening salvo in a larger campaign to weave financial functionality deep into iOS. Today, the Apple Wallet is a financial hub: a contactless payments tool, a secure credential vault, and a portal to Apple’s new high-yield savings account, all functioning within the company’s closed-loop ecosystem.

With Apple Pay Later, users can split purchases into four interest-free payments, financed not by a third party but by Apple Financial LLC. In just a few years, Apple has built a lending business, a savings product with billions in deposits, and one of the most used digital wallets in the world, all without a banking license.

However, what truly distinguishes Apple’s approach to fintech big tech convergence is integration. Apple doesn’t offer finance as a separate service; it embeds it within the user experience. Payments and savings become invisible, frictionless, and personalized. That’s where traditional banks fall behind.

Google: Infrastructure over interface

Google’s route into finance is less flashy, but equally potent. While Apple builds consumer-facing tools, Google lays the digital foundation for the next generation of financial systems.

Google Pay and Wallet are still widely used in many markets, storing everything from transit passes to loyalty cards. However, the deeper play is in cloud computing and artificial intelligence, technologies that power financial infrastructure across the industry.

Subscribe to our bi-weekly newsletter

Get the latest trends, insights, and strategies delivered straight to your inbox.

Google Cloud services are now integral to modern banking architecture. From KeyBank to Wells Fargo, major institutions are migrating core systems to Google’s environment, lured by promises of agility, cost reduction, and AI-driven insights.

Google doesn’t want to be a bank. But it wants to be the platform banks run on. This positioning is both strategic and defensive in the fintech big tech convergence. If tech firms can’t own the money, they’ll own the rails.

Amazon: The merchant’s bank of the future

If Apple owns the consumer, and Google owns the cloud, Amazon owns the transaction. E-commerce remains at its core, but around it has grown a quietly powerful financial ecosystem.

Amazon Pay competes directly with PayPal. Its BNPL offerings, in partnership with Affirm, are now default payment options for millions of users. But the real innovation is in merchant lending.

Through advanced data modeling and embedded finance tools, Amazon is offering working capital to small and medium sellers, often faster and more flexibly than banks.

And now, with its recent partnership with Parafin, Amazon is pioneering a new model of merchant cash advances. Repayment is based on revenue, so if a seller has a slow quarter, repayment slows too. It’s algorithmic empathy, scaled through data.

Amazon isn’t pretending to be a bank. But for many small businesses, it’s already something better: a partner who understands their revenue streams, credit risk, and customer demand in real time.

Yet this convergence isn’t without friction. Regulators are circling.

The Consumer Financial Protection Bureau has already expressed concern about how Apple and Google gate access to mobile payments. Meanwhile, Amazon’s growing financial footprint raises questions about data privacy, anti-competitive practices, and lending transparency.

To date, none of these companies has applied for a banking charter.

It’s likely they never will. Why would they?

They’ve found ways to operate adjacent to the regulatory perimeter—building banking-like services without assuming the regulatory burdens of a traditional institution.

But the longer the fintech-big tech convergence continues without complete oversight, the louder the calls for intervention will become.

Regulators will have to balance innovation with consumer protection without sacrificing the very technologies that are making finance more accessible.

Big tech in banking: What’s next?

Big Tech’s growing footprint in banking is reshaping how financial services are built, delivered, and consumed. As cloud-native infrastructure, AI, and data platforms become central to digital banking, the question is no longer if tech giants will influence the sector, but how deeply they’ll redefine it.

1. Superapps on the horizon

Elon Musk’s X has openly declared ambitions to become a financial hub. Meta’s Meta Pay is integrated across Facebook, Instagram, and WhatsApp. The age of the superapp is nearer than we think, even if the U.S. consumer isn’t fully there yet.

2. Infrastructure-as-a-service dominates

As banks continue migrating to Google Cloud and AWS, Big Tech will dominate the middle layer of finance, even if not licensed as banks. Infrastructure is the new battleground.

3. Embedded finance becomes the norm

From credit to insurance, expect more non-financial platforms to offer financial services. The line between bank and app will continue to blur.

4. GenAI rewrites the financial playbook

From chat-based financial assistants to algorithmic loan approvals, generative AI is reshaping user interaction. For CTOs, the challenge isn’t building AI, it’s deploying it safely, ethically, and scalably.

Will Big Tech replace banks?

A CTO’s critical crossroads in the new finance frontier

The question isn’t just if Big Tech is becoming the bank—it’s whether consumers want that future, and whether tech leaders are ready for the responsibility. Despite widespread access, sleek platforms, and unparalleled scale, support for Big Tech financial services is mixed, especially when trust and regulation come into play.

Apple, for instance, has transformed music, mobile, and computing—but its march into finance isn’t winning universal support. According to an Accenture survey, only 34% of millennials and 20% of Gen Xers would trust Apple’s financial services enough to bank with the company. That number drops further for older demographics. Interestingly, more millennials said they’d bank with Google or Amazon.

It suggests that even among digital natives, there’s caution when it comes to mixing consumer tech with core financial infrastructure.

Contrast this with PayPal, which earned the highest marks among non-bank players in the same study—garnering trust from 46% of millennials. It’s largely because of its focused value proposition, longer market tenure, and clearer role in the payments space.

So what does this divergence mean for CTOs navigating the evolving financial ecosystem?

Strategic implications for CTOs: Caution, capability, and consumer trust

For CTOs at traditional banks and fintech alike, the fintech big tech convergence is a double-edged sword:

- Capability isn’t the issue; trust is. Tech companies have the infrastructure, design acumen, and reach to offer financial services at scale. What’s harder to build is deep consumer trust around money, security, and identity, especially in light of Big Tech’s privacy track record.

- Speed matters, but so does resilience. Companies like Amazon, through Amazon Capital Services, are already disbursing loans based on seller performance data. Google Wallet links to banks, not balances. Apple Pay doesn’t (yet) store deposits. These companies are redefining banking by skirting the hardest parts: regulation, deposit insurance, and systemic risk. But that could also become their vulnerability.

- Regulation is the final frontier. With scrutiny from the CFPB and other regulators rising, CTOs need to think not just about innovation, but about regulatory navigation, ethical AI, and long-term sustainability.

The lessons from Alibaba and the looming Super app threat

Globally, we see the most mature version of this convergence in Alibaba’s Ant Group, which began as a payment provider and is now a financial ecosystem rivaling national banks, with $87 billion in holdings and over 80 million depositors. While not a licensed bank, Ant has blurred the lines so effectively that “for customers, it’s getting hard to tell the difference,” according to Accenture.

This model could become the blueprint for Google financial services, Amazon financial services, and even a more aggressive Apple financial services rollout in the future. But only if they can maintain the delicate balance between tech-first UX and bank-level trust and compliance.

CTO takeaway: Don’t compete, coordinate

For CTOs, the writing is clear: you don’t have to become a tech company, but you must build systems that operate in Big Tech ecosystems.

- Embed your services into super apps or partner APIs.

- Modularize your core banking stack to remain agile.

- Design for data privacy and transparency, or risk losing users to more transparent platforms.

- Be proactive in AI governance, especially when underwriting and financial nudging become AI-driven.

In a world where big tech in banking is no longer a theory but a timeline, CTOs must decide whether they want to be reactive and disrupted or embedded and essential.

In brief

A century ago, a bank was a building. Today, it may be a button or an invisible API in your checkout flow. The fintech big tech convergence redefines what it means to manage money. It challenges not just banks, but the broader tech and regulatory ecosystems to evolve. Google financial services, Apple financial services, and Amazon financial services are proof: Tech companies aren’t applying for banking charters, but they’re building what users now expect banks to be. For CTOs, the road ahead is clear, but complex. It’s not about chasing Big Tech. It’s about reimagining finance from the ground up. And that starts with code, design, security, and strategy, woven together into a financial experience worthy of the digital age.